AI regulation is taking shape across Asia. Governments are moving from voluntary guidance on usage toward binding rules that govern how AI is deployed in production environments.

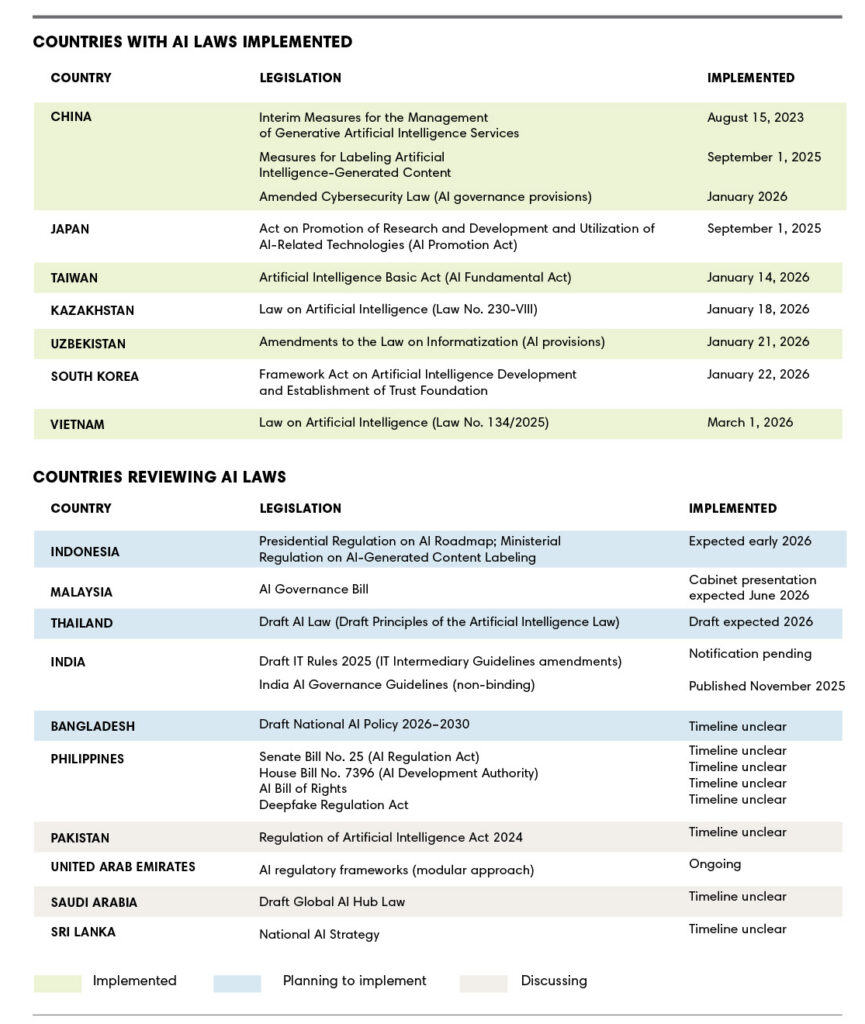

These rules intersect with ERP use cases in uneven and often indirect ways. In markets such as China, South Korea, and Vietnam, implemented AI laws regulate functions, including AI-generated content, high-impact decision support, and governance controls. Elsewhere in markets like India, Thailand, and Malaysia, draft or proposed rules point in a similar direction, though scope, timing, and enforcement remain unsettled.

While questions regarding whether vendors or users own compliance remain, legislation to date shows the importance of alignment between legal teams and system practitioners. That relationship appears set to influence ERP design and architecture decisions, as well as AI implementation choices. What is automated or AI-generated today creates workflow dependencies that may fall within new regulatory scopes tomorrow.

Convergence in Intent, Divergence in Execution

AI regulation is converging around a shared concern: how automated systems affect people, money, and regulated business activity. The way those concerns are translated into law, however, varies sharply by market, creating a fragmented compliance landscape.

Some jurisdictions are pursuing strong compliance-based regimes. In China, AI rules combine algorithm governance, content labeling, and data legitimacy requirements, establishing a high bar for systems that generate or rely on AI outputs.

Other markets adopted risk-based approaches that focus more on potential impact. In South Korea and Vietnam, obligations concentrate on “high-impact” use cases, particularly AI-based or -influenced decisions tied to employment, finance, or public interest.

A third group is still in flux. India, Thailand, and Malaysia have proposed or draft frameworks that signal future obligations, but leave scope, enforcement, and responsibility boundaries unsettled. By contrast, Japan and Singapore continue to rely largely on voluntary or sector-specific guidance, limiting direct ERP impact for now.

Labeling AI Output: Early Regulatory Signal

Labeling requirements for AI-generated content are one of the earliest and most concrete regulatory obligations emerging in Asia. These rules are narrowly framed, focusing on identifying AI-generated outputs, and their scope varies by jurisdiction and use case.

China has introduced the most explicit regime, requiring visible indicators and embedded metadata for certain AI-generated content. Labeling obligations also exist in Kazakhstan and Uzbekistan, though enforcement and practical application are still evolving.

Elsewhere, labeling remains more of a regulatory direction. Draft IT Rules in India propose visible labels for AI-generated content, while South Korea has introduced transparency and notification obligations for certain AI uses, with additional guidance forthcoming.

ERP systems are not the target of labeling rules. But labeling may apply to ERP workflows when AI-generated output moves from internal processes to formal records or communications. Identification and traceability have become key principles for regulators who are mandated to reinforce existing labor, tax, or finance laws.

High-Impact Decisions Reshape Finance, HR Modules

Risk-based rules governing high-impact decisions represent the clearest point where regulation begins to engage with enterprise workflows. These frameworks focus on decisions affecting employment, lending, and financial control.

South Korea’s AI framework defines high-impact uses by sector, including employment assessments and loan decisions. Requirements emphasize human oversight, explainability, and documentation.

Elsewhere, regulation is less direct. China does not use a dedicated high-impact framework, but algorithm governance and cybersecurity rules can still reach decision-support systems that materially influence regulated activities. Taiwan’s AI Basic Act signals a similar direction, establishing principles and anticipating risk classification, with specific obligations dependent on forthcoming sector guidance.

ERP systems are not the focus of these rules. Attention, where mandated, centers on workflows where AI influences outcomes for regulated activities. When AI-supported recommendations shape decision-making, those workflows may attract scrutiny under risk-based frameworks designed to reinforce existing governance obligations.

Documentation, Explainability, Audit Trails

Documentation and explainability are increasingly treated as design assumptions. Where AI influences regulated decisions, organizations may be expected to explain outcomes, show where human judgment intervened, and reconstruct decision paths if challenged.

In ERP environments, this shifts attention to workflow design. AI-supported recommendations that affect finance, HR, or compliance activities may require built-in decision logs, review points, and evidence of human intervention. These requirements are not universal, but when they apply, they shape workflow construction.

Early examples of this regulatory interest can be seen in South Korea’s high-impact AI rules and Vietnam’s emerging conformity requirements. Taiwan’s AI Basic Act points in a similar direction through principle-based obligations that will be defined by sector regulators.

Among emerging control areas, this intersects most directly with ERP because these systems serve as systems of record. AI-supported outputs can flow directly into financial close, compliance reporting, and operational execution. In markets with documentation and explainability requirements, organizations will need to ensure they can justify how AI-influenced decisions are logged, reviewed, and governed at design time.

ERP Governance for Uneven AI Regulation

While AI regulation is developing unevenly across Asia, the direction of travel is becoming clearer. Rules increasingly focus on how AI is used in production, how it shapes regulated decisions, and whether organizations can explain its effects. In that context, preparation means understanding where ERP design choices may create future regulatory exposure.

Several practical questions can help frame an initial assessment:

- Does the ERP generate AI content that must be identified or traced?

- Does AI influence decisions tied to rights, money, or employment?

- Can outcomes be explained and documented for audit?

- Who owns compliance when AI is embedded—vendor, customer, or both?

- Can governance adapt as rules diverge across jurisdictions?

Early guidance suggests organizations benefit from auditing where AI is embedded across ERP modules, clarifying governance frameworks, and engaging vendors early to align on documentation, update cycles, and responsibility boundaries.

These steps do not eliminate uncertainty. They do, however, reduce the risk that routine ERP workflows accumulate AI dependencies that fall into regulatory scope later.

What This Means for ERP Insiders

ERP risk emerges from use, not deployment. AI regulation across Asia is not triggered by installing new ERP features, but by how those features are used over time. As AI shifts from optional assistance to embedded workflow logic, ordinary configuration choices can quietly convert internal processes into regulated decision pathways.

Regulatory divergence favors adaptable ERP architectures. AI laws in Asia are aligning on intent but diverging in execution, timelines, and scope. This rewards ERP environments designed for modular governance—where AI capabilities, controls, and documentation can be adjusted locally—over globally standardized implementations that assume uniform regulatory treatment.

Governance maturity will outpace legal certainty. Clear legal boundaries around AI responsibility remain elusive, particularly between vendors and users. Organizations that wait for definitive rules risk retrofitting controls too late. Those that treat explainability, traceability, and oversight as design principles gain resilience as regulation hardens unevenly.