Most ERP projects do not fail during implementation. The cracks tend to appear later, a year or two after go-live, when the business grows, the structure becomes more complex, expansion adds entities or geographies, or new reporting requirements emerge. At that point, the system technically works; however, answering key management questions takes longer, reports require increasing manual adjustments, and even small changes become costly.

These issues are often attributed to ERP limitations, the wrong vendor choice, or missing functionality. In practice, the root cause usually lies deeper. Long-term outcomes are shaped by financial architecture decisions made before and during implementation. In particular, by the chart of accounts structure, the logic of dimensions, and the approach to entities and reporting.

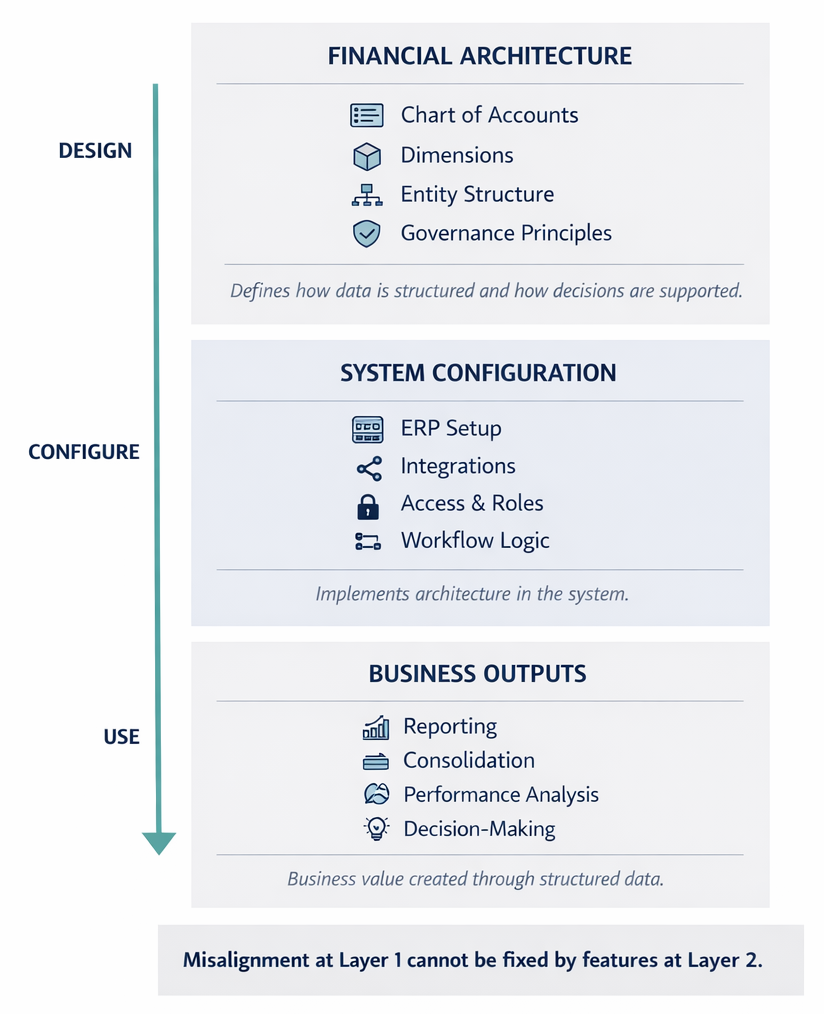

ERP functionality can evolve over time. Financial architecture, once embedded, often remains for years, either supporting scale or constraining it.

This is where many ERP discussions lose focus. Instead of starting with management logic and data structure, they move quickly to system capabilities. ERP then gets treated as the driver of success, when in practice it executes decisions made at the architectural level. That distinction matters because many limitations that surface later are not product failures. They are the result of structural choices the system was asked to formalize.

Separating these two layers—ERP as a system and financial architecture as a data model for management—changes how long-term limitations are understood. Many limitations that surface later are not product failures, but the result of structural choices the system was forced to formalize.

ERP Functionality vs. Financial Architecture

ERP selection almost always begins with functionality. Interfaces, modules, out-of-the-box reports, automation and integration capabilities are compared side by side. This is understandable: features are visible and measurable.

However, a more fundamental layer of decision-making is often overlooked.

ERP processes data. Financial architecture determines what data enters the system, how it is structured, and which management conclusions can be drawn from it. Two companies can use the same ERP platform and experience completely different levels of transparency and control, depending on how their chart of accounts, dimensions, and entity structures are designed.

ERP focuses on:

- how transactions are processed

- how workflows are automated

- how modules integrate.

Financial architecture defines:

- what data enters the system

- how it is structured

- which management questions can be answered.

Architectural decisions are frequently treated as secondary and postponed in favor of speed. The assumption is that adjustments can be made after go-live. In reality, these early decisions create long-term constraints. Features can be added and reports rewritten, but rebuilding financial architecture years later usually requires significant effort and disrupts data comparability. It can also slow close cycles, complicate consolidation, and make profitability analysis harder to trust across business units or regions.

In resilient ERP projects, the more useful question is not “What can the system do?” but “What financial model must the system support today and in the years ahead?”

Chart of Accounts: More Than an Accounting Requirement

The chart of accounts is often seen as a technical accounting tool required for compliance and reporting. In the context of ERP, it plays a much more structural role. It forms the backbone of financial architecture, shaping not only how transactions are recorded but also which management questions can be answered without manual workarounds.

Two common design extremes illustrate the problem:

- Replicating a legacy chart of accounts without rethinking its relevance to the current business model

- Over-engineering the structure by creating a new account for every operational nuance.

In the first case, the structure becomes disconnected from how the business actually operates. In the second, it grows increasingly complex and rigid, making cross-period and cross-segment comparison more difficult. Both approaches create problems for scale: one limits visibility, the other limits adaptability.

This is particularly visible in Advertising and Promotion (A&P) expenses. The desire for detailed analysis often leads to creating separate accounts for every campaign type, platform, or channel. As digital tools evolve, the account structure often expands faster than the business itself.

Detailed A&P analysis is indeed important. However, it is better handled through dimensions, BI tools, or specialized marketing systems. In this approach, the chart of accounts remains stable, while flexibility shifts to the analytical layer, where changes can occur without disrupting the structural foundation.

Get Our Free Weekly Newsletter

Dimensions: Where ERP Value Is Actually Created

If the chart of accounts provides structural stability, dimensions introduce analytical depth and flexibility.

Dimensions are not merely technical ERP settings. They are deliberate data views that allow management to analyze performance across products, channels, regions, projects, or other business drivers without modifying the core accounting structure.

Poorly designed dimensions create two types of risk. If too few dimensions are introduced, analytical visibility remains limited and teams revert to manual reporting. If too many are added without clear logic and ownership, reporting becomes inconsistent and difficult to interpret.

The objective is not to maximize the number of dimensions, but to design them around meaningful management questions. When done correctly, dimensions allow businesses to expand product lines, enter new geographies, or introduce new channels without constantly restructuring the chart of accounts.

This is where ERP value becomes more visible. It emerges where structural stability and analytical flexibility are intentionally aligned and designed to work together, not when one is asked to compensate for the other.

Entities and Structure: Designing for Change, Not Stability

Beyond the chart of accounts and dimensions, financial architecture also includes the structure of legal and managerial entities. Decisions about how companies are organized within a group, how responsibilities are allocated, and how consolidation logic is defined directly influence the long-term resilience of the ERP model.

During implementation, the existing structure is often treated as a fixed starting point. The system is configured around the current organizational model, which appears stable and sufficient. In practice, however, organizational structures evolve more frequently than expected.

A company may separate its e-commerce operations into a standalone legal entity to improve operational transparency or optimize taxation. If such scenarios were not considered during architectural design, reporting structures, cost allocation logic, and historical comparability can quickly become inconsistent. In larger enterprises, the same issue can complicate shared services, internal charging models, and post-acquisition integration.

Even well-designed architectures will require adaptation over time. Growth, regulatory changes, and strategic shifts inevitably affect the entity structure. The question is not whether change will occur, but whether the system can absorb it without structural disruption.

A resilient financial architecture does not eliminate change. It limits its consequences. Adding a new entity or adjusting the group structure should not require rebuilding the chart of accounts or redefining reporting logic. When architecture is designed with evolution in mind, organizational transformation becomes manageable rather than destabilizing.

Sponsor Industry‑Grade Research

Who Should Own Financial Architecture Decisions

Financial architecture decisions cannot be treated as purely technical configuration choices. They define how performance is measured, how accountability is structured, and how management decisions are supported.

In practice, ownership is often blurred. IT teams and system integrators focus on system logic and technical consistency. Finance, procurement, operations, and sales focus on usability and business outcomes. When architectural decisions are made without clear ownership, the consequences surface only after go-live.

For example, deeply embedded configuration logic in purchase order workflows can create unintended rigidity. A seemingly minor adjustment by finance may trigger document reversals or workflow resets, not because the system is flawed, but because user roles and modification rights were not designed with business realities in mind.

These issues are rarely visible during technical testing. They emerge when real operational scenarios begin to unfold. At that stage, adjustments become significantly more expensive and disruptive.

Ownership does not mean finance should dictate technical configuration. It means finance must define the structural principles: the chart of accounts, dimension logic, reporting requirements, and the boundaries of flexibility. Technical teams implement these principles. When this separation is clear, implementation becomes collaborative rather than adversarial.

Practical Checklist: Questions to Ask Before ERP Implementation

Before starting an ERP implementation, it is useful to pause and clarify the architectural logic behind the system.

A few questions can significantly reduce long-term complexity:

- What management decisions should this structure support in two to three years?

- Which dimensions are truly necessary, and why?

- How might the entity structure evolve as the business grows?

- Which structural principles must remain stable over time?

- Who owns architectural decisions, beyond technical configuration?

- Where are we prioritizing speed over structural clarity?

Clarifying these points early reduces the risk of embedding structural constraints into the system before the organization fully understands their long-term cost.

ERP implementation is a project with defined timelines and milestones. Financial architecture is the operating model that will shape decision-making long after the project is completed.

When these two layers are treated as separate discussions, alignment usually gets harder as the project moves forward. When architectural decisions are postponed until late in the implementation, the consequences rarely stay contained within the project itself. They tend to surface later in reporting complexity, governance friction, and expansive workarounds.

Clarity in ERP systems depends on the structure defined before configuration begins. In practice, the system ends up formalizing whatever logic the organization has already chosen, whether intentionally or by default. That is why scale, flexibility, and management clarity should be determined before configuration begins—taking the time to define these principles early makes later decisions far less reactive.

Editor’s Note: What This Means for ERP Insiders

Financial architecture is a more decisive factor in ERP success than feature breadth alone. Vendors and implementation leaders often compete on automation, usability, and module depth, but those advantages weaken quickly when the underlying chart of accounts, dimensions, and entity logic cannot support how the business is actually managed. The long-term differentiator is not whether a platform can process transactions, but whether the financial model embedded in it can absorb growth, complexity, and change without constant redesign.

Scalability depends on preserving structural stability while creating analytical flexibility. That is why decisions about dimensions, reporting layers, and entity design carry outsized weight; they determine whether new products, geographies, business units, or legal structures can be introduced without breaking comparability or forcing manual workarounds. Systems become harder to govern when organizations use features to compensate for weak structural decisions made earlier in the project.

Governance ownership is an underappreciated determinant of ERP resilience. When financial architecture is treated as a technical setup issue rather than a business design decision, organizations often discover the consequences only after go-live, when reporting friction, workflow rigidity, and costly adjustments begin to surface. The strongest ERP programs are not defined only by smooth deployments, but by early decisions that keep finance, operations, and system design aligned as the business evolves.